Ryan Loehr

March 11, 2021

Craig, Tim and I recently attended an investment conference on the Gold Coast. A two-day event bringing together a number of reputable Australian Advice firms, portfolio and research managers to discuss the changing investment, regulatory and advice landscape and what it means for clients.

In the opening address, the Chair of the conference referred to a recent visit he and his children had made to Dreamworld and drew a comparison between our role and that of a Roller-Coaster operator. “Client portfolios can have big highs, lows, twists and turns and it is our job is to ensure that each participant remains seated for the duration of their ride. The only difference is, we don’t have a mechanical harness to keep clients from exiting too early.”

While the thought of investment ‘roller coasting’ may sound alarming, it shouldn’t be. Corporate profitability has and will continue to change through different market cycles, with peaks, troughs, positive and negative surprises all of which cause short-term market prices to fluctuate. We should be glad for this volatility because these ups and downs are the reason that equity (share market) returns have historically been better relative to almost any alternative asset class.

In 2020, our client portfolios achieved exceptional returns. Despite the February low, we are pleased to say that all but one of our clients ‘remained seated’ for the year and markets reached record highs – despite a global pandemic and the ‘worst economic recession since the great depression’ (IMF, April 2020).

Fast-forward to 2021 and on the tip of everyone’s tongue is ‘what’s next?’

In recent weeks we have witnessed a spike in volatility, but interestingly, this time it has started within Government Bonds. I say ‘interestingly’ because Government bonds are viewed as the ‘risk-free’ rate of return and yet the Australian Bloomberg Ausbond Composite Bond Index just finished its worst monthly return in history, with February down -3.59% as bonds crumbled.

The Australian 10-year government bond flash crashed with yields at one point last week spiking almost 90bps versus the start of February — one of the biggest moves ever. (Franklin Templeton Fixed Income Team, March 3 2021).

This volatility occurs in bonds because the expectation for a rise in interest rates makes existing debt on issue less attractive. If I purchase a government bond that pays me 1.00% in interest annually, but then the following year the Reserve Bank issue new bonds with rates at 1.50% it would make my older bond worth relatively less if I were to try and resell it back to the market before it matures.

Australian Government and Global Developed Government Bonds are typically seen as setting the ‘risk free’ rate of return for investors. This is because it gives investors an IOU like instrument from the Government that is seen as the most secure creditor available. Despite market volatility like the above, if held to maturity, the bonds repay the both principal and interested promised.

Yet, this risk-free’ rate of return isn’t always risk-free. The current low yield on offer (net of forecast inflation for 2021) for shorter-term bonds (<5-years) is negative; any need to exit the bond before maturity is subject to capital value fluctuation (like the above) and foreign bonds also have currency risk attached.

Many of our clients will note our logic to keep underweight bonds in 2020 Q3 & Q4 reviews where we stated:

“We are underweight fixed-income based on their low-yields and the potential for government stimulus to become inflationary. Higher inflation could erode the capital value of existing bonds because the new debt would be issued with higher rates. We are revisiting fixed income more broadly and what constitutes a ‘defensive asset’, while still providing a level of income practical for our clients’ needs.”

In terms of where the biggest risks are in fixed income, this has been in long-duration instruments like the 10-year government bond. It is perfectly reasonable to expect that interest rates may rise over the next decade, as the Covid-19 recover continues; we have successful vaccine rollout; and there is economic normalization. The market is simply pricing in this reality. Yet, in the shorter-term the Reserve Bank of Australia (and other major central banks) have kept a commitment to low rates for at least the next 3-years; and in the RBAs case, the logic follows in the types of bonds it has been purchasing (3-year).

Bond yields (and inflation) matter for equities, because rising rates mean that companies with a high price relative to their earnings, or those with significant borrowings me be impacted by the cost of capital increasing:

In recent weeks, we have seen significant market flows out of companies trading at above average earnings multiples in the so called ‘reflation trade.’

The idea is that with inflation and economic growth picking up sooner than expected, central banks will be forced to increase rates sooner to prevent markets from overheating. This could undermine the attractiveness of some sectors, such as technology stocks, which enjoyed outstanding returns in 2020, but by historic levels now appear expensive. Instead, the argument is that favoring ‘value stocks’ or those that significantly under-performed in 2020 which may give investors a better source of return as their profitability recovers.

I wanted to touch on the growth vs. value distinction because 1. it’s very topical right now and 2. we think these simplistic labels mislead investors.

‘Growth’ is viewed as a forward-looking approach, seeking out companies that can grow their earnings in the foreseeable future and continue growing them rapidly.

‘Value’ is usually viewed by some historic perspective, where a company is trading at a discount to some intrinsic value. Value investors buy these stocks “cheaply” when investors have reacted to some short-term news and then wait for the price to revert to the historic mean.

We believe that this idea of margin-of-safety or mean-reversion favoured by value investors of old may not be useful anymore. Companies can grow at unprecedented rates at little marginal cost. Intangible assets such as intellectual property, networks and data can be the main determinants of future cash-flows. These assets can create increasing returns of scale and a winner-takes-all dynamic, capturing market share from these old-world companies, emerges.

As an example, why would oil company shares revert to the mean (long term average) if renewable energy is becoming both cheaper and storable? Why would physical retail stores revert to mean trading levels when more people prefer shopping online? Why would office property rents revert to the mean if large corporates encourage remote working arrangements and staff are more productive/prefer working from home?

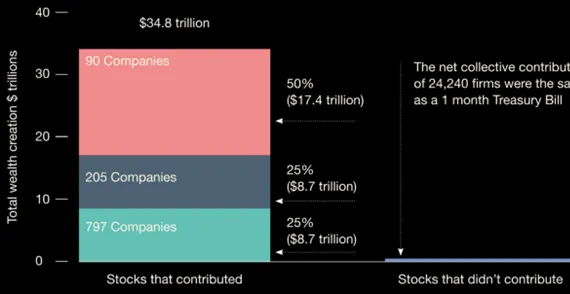

As one of our Fund Managers, Baillie Gifford has highlighted, history shows that the vast majority of long-term wealth creation in stock markets comes from a vanishingly small number of explosive winners. So, ‘Growth or Value?’ isn’t the right question anymore. Both may fail as investment strategies — in index terms — when compared to the much narrower questions for exponential scale. The real question ought to be ‘how do we find the top ~5% of companies that will drive most of the market return, as illustrated by the below.

Academic research has shown that from 1926 to 2016, a mere 90 companies were responsible for half of the $35 trillion of wealth created by US equities.

Reading the data: The data includes all 25,967 CRSP common stocks (25,332 companies) from 1926 to 2016. Beyond the best-performing 1,092 companies, an additional 9,579 (37.8%) created positive wealth over their lifetimes, just offset by the wealth destruction of the remaining 14,661 (57.9% of total) firms. The implication is that just 4.3% of firms collectively account for all of the net wealth creation in the US stock market since 1926.

We care less about whether a company is ‘growth’ or ‘value’ and more about the quality of the company, the ability for it to compound earnings, increase its scale and ability to maintain a sustainable competitive advantage. As long-term investors, our role is remain seated for the journey of the ride, supporting the top 5% of companies that will deliver outstanding returns and not get distracted by the noise of short-term speculative traders proclaiming growth or value.

I hope you have enjoyed this note. Keep a look out for Craig or Tim’s next update in two weeks’ time.

Any questions please don’t hesitate to contact either Craig, Tim or myself.

Regards,

Ryan Loehr

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

NewsLetter

Free Download