Charles Troian

April 11, 2025

In Wall Street: Money Never Sleeps (2010), a reformed, or perhaps just rebranded, Gordon Gekko famously declares that “Speculation is the mother of all evil.” Coming from the man who once glorified greed, it was a jarring pivot, but Gekko had a point. And if you’ve been watching markets lately, it’s hard not to feel like we’re back in the speculative soup.

Trying to trade this market is trying to predict the psychology of Donald Trump: erratic, attention-grabbing, and entirely untethered from economic reality. Is inflation cooling? Is the Fed coming to the rescue? Was the imposition of ‘Liberation Day’ tariffs unconstitutional? Did Trump really just post an AI generated video of him and Elon eating lobster on the Gaza strip?

As private wealth advisors, we are often expected to have the answers to these questions, but with the constant retraction of statements and the erratic decisions of the President, I’d posit that the questions the market currently speculates on are at best, hypothetical. Over the last week, I have spent several hours on the phone with clients pondering the mind of DJT. In retrospect, this has been an exercise in futility – of all the likely outcomes, I did not expect Trump to swallow his pride and soften his stance so soon, as he did overnight. The outcome? We were quickly reminded just how fast markets can move upwards. The lesson? Prepare for volatility, do not react. At EW&L, we are not making high-conviction bets on short-term headlines. Aggressive portfolio re-balancing in this environment is akin to the game of musical chairs, and if you get it wrong, you’ll end up on your rear dazed and confused. So why play?

Whilst we aren’t forced to react, we do need to stay awake at the wheel and try to make sense of the world. Alas, another day has been forced upon us where we must attempt to rationalise the irrational. In this note, I will attempt to make sense of Trump’s hard ball stance on Tariffs, and why he thinks tariff’ “is the most beautiful word in the dictionary”.

THE ELEPHANT AND THE GLORIFIED BOND SALESMAN

When it comes to the health of the US and global economy, it’s fair to say that US Debt is the elephant in the room. Whilst Trump’s first term was polarised by an obsession with stock market performance, his second term has not followed suit… at least for now. Instead, in all his patriotism, he has decided to hunt the ‘elephant’, and in the process become a martyr for financial markets.

In 2012, national debt stood at $11.4 trillion USD and approximately 69.5% of GDP. Today, it stands at around $28 trillion USD, or approximately 99% of GDP. The Congressional Budget Office (CBO) projects that interest payments on this debt will total $952 billion in fiscal year 2025 and rise rapidly throughout the next decade. Scary stuff, but what has this got to do with Tariffs? The answer is everything (maybe) – something we can be more confident in given Trump’s back pedalling overnight.

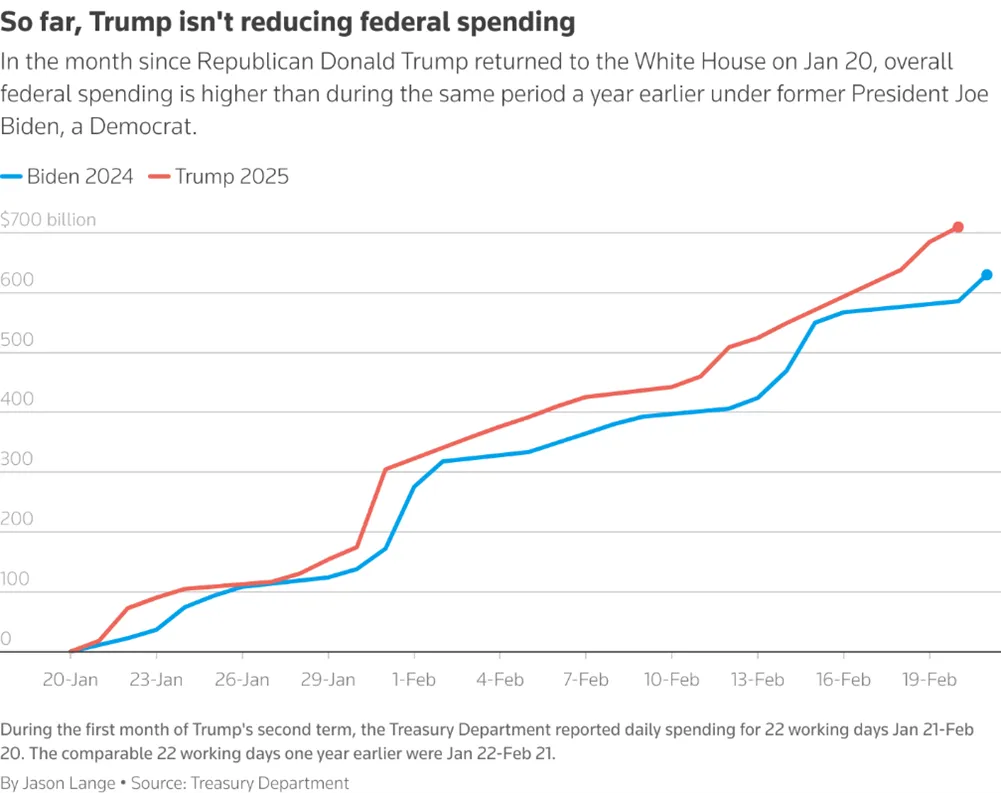

Leading into the year, markets were awash with optimism, Trump 2.0 promised to bring corporate tax cuts, de-regulation, onshoring, and ultimately restore the US to its glory days as a manufacturing powerhouse, all the while reducing ballooning government debt. How do you do the latter when cutting personal and corporate tax rates? You impose taxes on the rest of the world in the form of tariffs and make them foot the bill, or so DJT’s theory goes. Or conversely (or in combination), you reduce government spending. However, despite the noise created by the Department of Government Efficiency (DOGE), freezing billions of dollars in foreign aid, and firing 20,000 federal workers, US government spending clocked in at $710 billion USD between January and February, up circa 13% YoY. Thus, it can be inferred that tariffs will need to do some heavy lifting towards making a dent in government debt. Early analysis by economists suggests that the revenue generated by ‘Liberation Day’ tariffs (paused overnight), will do little to clip even a portion of the US Treasuries interest repayments, let alone the principal. So then, what’s really the deal with Tariffs, short of the classic form of political showmanship we have come to love (or hate) from the Don?

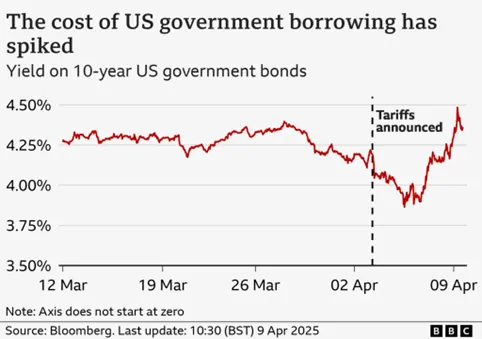

The US Treasury is staring down the barrel at ~$8 trillion USD in debt maturing this year that it will need to re-finance. Unlike us regular civilians with credit cards, the US Treasury cannot do a balance transfer and strategise to pay down the debt during a 0% honeymoon period. Instead, they need to re-finance at a rate generally pegged to the 10 Year UST Bond Yield as a proxy. This is where we go down the rabbit hole, for argument’s sake, and speculate on the strategy at play by Trump and his advisor Scott Bessent, the US Secretary of Treasury.

Towards the back end of last week, we witnessed 10 Year UST Bond Yields nosedive as equity markets sold off following ‘Liberation Day’. Trump disregarded declines in equity markets and remarked that there would be necessary pain as the world re-calibrates towards his economic vision. As spooked money exited the stock market, investors seemingly pivoted into safe-haven assets such as government bonds, forcing the price of bonds up and their respective yields down. Was this a mere coincidence or a masterful orchestration to force rates lower, without the helping hand of J Powell and the good folk at the Federal Reserve? The answer really depends on how much credit you want to give him but nonetheless is a moot point – as it were, this strategy (if no mere coincidence), backfired. The markets ultimate response to Trump’s creation of significant financial risk has been to signal a reluctance to purchase US government debt. As a result, bond prices started cratering, which caused a sharp increase in effective interest rates, as observed in the graph below. This outcome is directly contrary to Trump’s stated goal of significantly lowering US interest rates. In bond markets, reducing interest rates requires the confidence of investors (more buyers than sellers). Undermining that trust by deterring potential buyers of US debt has the opposite effect.

Despite the White House’ insistence that bond market volatility had no role in Trump’s 90 day pause on Tariffs, his reversal in tune came at a time of great convenience. If disruption of this magnitude continued, it’s likely that the Federal Reserve would have needed to step in with a circuit breaker and purchase bonds to stabilise the market – something that hasn’t happened since the Covid Era market chaos in 2020.

In their defence, Bessent has suggested that volatility is not a function of dwindling US confidence, but rather a result of hedge funds de-leveraging their basis trade strategy’s.

The basis trade strategy involves borrowing substantial sums to exploit minute pricing inefficiencies between U.S. Treasuries and their corresponding futures contracts. In ordinary times, such trades provide vital liquidity and efficiency to money markets, acting as a lubricant that keeps the financial system running smoothly.

However, when the scale of this trade reaches eye-watering levels – estimated at around $1 trillion USD – the unwind can send shockwaves through the bond market. As funds exit these positions en masse, the market is forced to absorb an outsized influx of Treasuries. This sudden increase in supply can drive yields sharply higher, reflecting the market’s struggle to digest the excess without the usual leveraged demand.

While unsettling in the short term, Bessent’s view is that this process is part of the natural rebalancing mechanism in financial markets – one that ultimately restores stability and sets the stage for more sustainable market conditions.

Naturally, this is the view and response I’d expect from a self-described ‘glorified bond salesman’. In my opinion however, whilst basis trades may well form a part of the problem, it’s hard not to ignore the multiplier effect of stirring the pot with the buyers of your bonds. Alarmingly, 30% of debt issuance is owned by foreigners. Take China for example, who Trump generously awarded with 125% tariffs, and consider for a moment that they own some $759 billion USD in US Treasuries. It’s hard not to make the argument that Trump’s trade war is undermining the US Debt market, and this may ultimately strong arm him into a more diplomatic approach with trade partners – the beginning of which we saw on Wednesday night with his 90 day pause. Even the resolute and pigheaded POTUS is forced to bow down to the bond market, and this should give investors some confidence that his powers are in check by Mr Market.

“I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a 400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.” – James Carville, Chief Strategist to Bill Clinton

INFLATION, GROWTH, AND INTEREST RATES - THE THREE MUSKETEERS OF MARKET DIRECTION

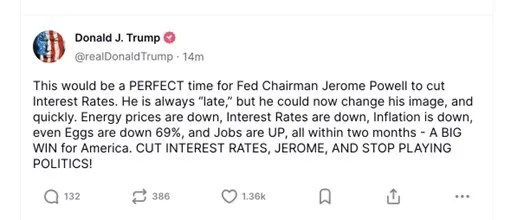

In his conquest to lower rates, Trump has long clashed horns with his personal adversary in Jerome Powell. Naturally, the independent nature of the Federal Reserve has long rubbed Trump the wrong way, where his all-caps-lock tweets fail to have influence. The Fed has two primary objectives: to keep inflation within target and to promote maximum employment. For someone tasked with these duties, life just got a hell of a lot harder.

The pervasiveness of Trump’s Tariffs is expected to impact US growth, and at least in the first instance, prove to be transitorily inflationary. To what degree? Both are unknown.

Powell has affirmed the Central Bank’s independence and stated they will not come to the rescue with a ‘Fed Put’. The Fed cannot afford to act with haste as it contends with the difficulty of navigating both the inflationary and recessionary impacts of a global trade war. Moreover, the Fed cannot set a precedent that they will bend to Trumps manufactured market chaos to force their hand. So, what does this mean for markets and client portfolios?

Buckle up. The futures market is now forecasting 3-4 rate cuts by central banks by year end, both domestically and in the US. Whilst we aren’t broadly fans of forecasting at EW&L, we view the risk to the outlook as requiring central bank intervention at some point (soon), with more short-term pain before then. There are two probable scenarios as they relate to growth, inflation, and the cash rate direction.

In any instance, we expect a tug-of-war to play out between Trump and his trade partners, and all the while Trump will be playing the same game with Jerome Powell. The moderator of these contests will be the US Debt market. Expect more grandstanding, expect more market volatility, but trust in the benefits of diversification and respect the danger inherent in speculation. We don’t know where things are headed in the short term, but we have positioned client portfolios defensively to weather the storm. Over the last quarter, we have de-risked portfolios to include greater exposure to defensive equities (value/infrastructure/property) and uncorrelated alternatives. Broadly, we are well positioned to capitalise on dislocations that have arisen amidst current market instability, and portfolios remain well insulated from the brunt of the headline making sell offs.

We’re not merely navigating an economic cycle or a political moment – we’re contending with an entire paradigm of unpredictability. From tariff-induced turmoil to debt market tremors, the signals are mixed, and the noise can be deafening. Yet amid the cacophony, our role as an adviser remains constant: to rise above the speculation, remain grounded in fundamentals, and guide clients with a steady hand. As we peer through the fog of uncertainty, I’ll leave you with one last quote from Wall Street: Money Never Sleeps (2010), that rings true when I think about those running our economic and global affairs.

“Maybe I was in prison too long. But sometimes it's the only place to stay sane and look out through those bars and say, 'Hey! Is everybody out there nuts?’” – Gordon Gekko

Until Next Time,

Charles

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

NewsLetter

Free Download