Tim Whybourne

January 3, 2022

During the session we all spoke about why we are in this business, what drives us and who it is that we are helping.

I love what I do, knowing what we do makes a material difference to the lives of our clients, and that the right strategy now can make a huge difference to our clients’ lifestyles and their family’s lives, sometimes for generations to come.

A particular case study came to mind in two friends that we started talking to about 15 years ago. One of them came on as a client and one of them did not, however we have been speaking to them both ever since.

For the client, we provided sensible advice to start considering super whilst the friend did not. The difference over 15 years (with two similar levels of income) has amassed to a few million dollars. Obviously, it’s hard to do a direct comparison but I have no doubt that at least some of that difference is a result of a solid strategy for our client.

The point is, I have seen what prudent financial advice can do for a client over time and how making small changes now can result in disproportionate benefit down the track.

This is one of the reasons I have no problem getting up in the morning. I love what I do!

The investment options in your superannuation actually don’t differ from what you can invest in outside of super.

You still have the option to invest in asset classes that you choose – from listed equities, both domestic and international bonds, both domestic and international currencies, cryptocurrencies, venture capital, private equity, art and even wine or rare cars.

However, there are a lot of different rules that apply for holding these lifestyle-type assets in your super versus outside of your super. If you do hold these inside your super, you are unable to derive any personal benefit from your superannuation investment.

The sole purpose of all your super investments must be to provide for retirement – not for current enjoyment.

The fact is, we are all getting older and older and we’re all actually expected to live longer and longer as the years go by.

So, what may have been an acceptable superannuation balance 20 years ago is likely not going to be sufficient for today’s retirees – especially when you account for inflation.

There is a misconception – particularly in young people – that they don’t need to worry about superannuation because retirement is so far away. But that couldn’t be further from the truth.

The biggest benefit that young people have is time on their side. The more years you have to compound a return in superannuation, the more powerful the effect of compounding returns can be.

The biggest risk of investing in super:

The biggest risk investors face is putting money into their super too early or committing some capital into superannuation and then needing that money before they retire further down the track.

The fact is, once your money is in super, you cannot take it out unless you meet one of the conditions of release. For most people, this is when they meet the age test requirements. The age you can access your super varies depending on your date of birth but if you were born after the mid-60s it’s approximately at the age of 60.

The second biggest risk of investing in super:

The second biggest risk that people talk about is regulation risk.

Currently, superannuation contributions are taxed at 15% under our present rules. However, the government could always change those rules to make it less appealing which has some people fearful of investing in super.

There are also rules about how much money you can contribute to your super fund.

If you don’t get good financial advice about putting money into your super, you may breach one of those rules. The penalty for this can actually be quite severe so it’s important to be aware and careful.

While changing government regulation is always a risk, it is extremely unlikely that the government would make it less beneficial to invest in your super.

It’s in the government’s best interests to allow people to contribute to their super in a financially beneficial way so that our population doesn’t become a burden on the public system when they retire.

Our government is always going to try to incentivise people to put money into their super – and the only lever they have to do that is a lower tax environment.

This is an impossible question to answer because it’s different for everyone.

I think the government has a very basic definition of how much you need to retire and what your daily living allowance needs to be. According to the government, this number is about 45k per annum (ASFA Retirement Standard – Moneysmart.gov.au).

This is what the government thinks a single person can survive on comfortably. But it’s certainly not the case for most of the clients that we deal with.

If you are thinking about investing for the long-term and you definitely don’t need the money back any time soon, the best vehicle for that is always going to be your superannuation because it’s the lowest tax environment.

One of the most common misconceptions we hear about investing in super is that salary-sacrificing is only worthwhile for high-income earners, which just simply isn’t the case.

The fact is, if you’re taxed at more than 15% personally or in any other vehicle, then you will likely benefit from salary sacrificing.

The most obvious benefit of contributing to your superannuation is that you pay less income tax.

There are things called concessional and non-concessional contributions.

Concessional contributions are the contributions that your employer will pay into your fund – and they come as a tax deduction to yourself.

As an example, if your employer put $10,000 into your superannuation fund as part of your pay package, you would still be left with the option to put additional money into your superannuation funds which would come with a tax deduction to you. These funds would go in taxed at 15% (up to the current concessional tax limit which is currently $27,500).

The other clear benefit of super investing is that you pay less on the investment returns.

For any income or capital gains that you have generated in your superannuation fund, you will only pay a maximum of 15% tax on that income – which can really compound over time.

Another benefit is that any funds in your superannuation are actually protected against bankruptcy. It’s not a common concern that most people have, but if you run a business, sometimes bankruptcy is outside of your control. However, if you have your money invested in super, it is typically protected (there are exceptions to this).

The other big benefit is being able to enjoy a tax-free income when you retire.

We have a lot of clients that were able to put a lot of money into super when the government was allowing you to put up to a million dollars in one payment.

If you made this contribution 20 years ago and have been making good super returns, your super fund may be worth north of $10 million today.

These clients are able to pull out a tax-free income in retirement as a result of that.

The final benefit of superannuation we will highlight is that it doesn’t actually form part of your estate when you die so you can choose who your superannuation benefit goes to through a binding death benefit nomination.

The simple answer to this is as early as possible.

As soon as you start working, your employers have to start putting a mandatory amount into your superannuation fund.

However, we always encourage our clients to think about contributing more on top of these payments.

Even something that can seem relatively insignificant to you now – for example, $100 a month – could be incredibly beneficial because:

We often meet clients in their 50s, 60s, or even 70s who haven’t thought about superannuation and it’s still a strategy that we look at for them if they have access to other funds outside of the superannuation environment and if they are below those superannuation caps.

We don’t encourage people to look at their superannuation balances or investment balances too frequently.

Looking at your superannuation frequently may make you feel like you need to make drastic changes.

However, we remind our clients that super is a long-term investment. So, it’s not something that you need to look at frequently.

But if you are in an industry fund, it would be beneficial to review that fund and ideally, talk to a financial advisor about that.

In my opinion, reviewing your super fund on an annual basis can help you determine whether you’re in the right investment options for you, whether you should be putting more money into super and whether you’re on track to meet your goals.

When we typically meet clients, they have one of two vehicles:

For me, one of the most powerful things about superannuation is the tax environment and the difference that can make over time.

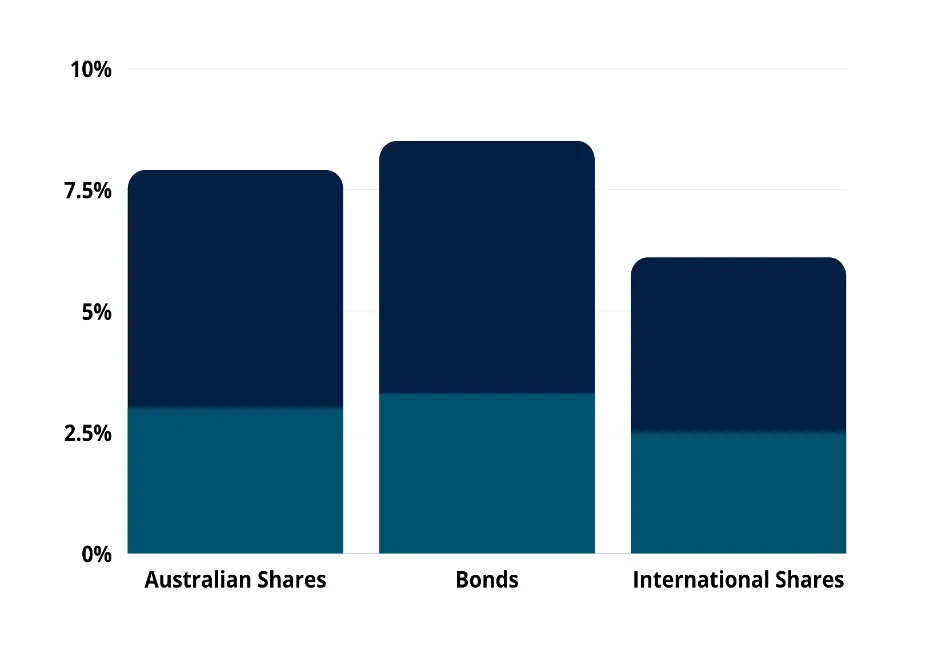

I came across a study that showed the different investment returns in over 10 years when you invested inside of your super versus outside of your super.

To give you an example of the power of superannuation investments, the graph below demonstrates the after-tax returns across three simple asset classes.

(Source: 2017 Russell Investments /ASX Long Term Investing Report)

To illustrate this point, we designed a hypothetical portfolio – a basic portfolio with 60% shares and 40% bonds. Of the 60% of shares, half were Australian and half were international. What we found was that if you invested $100,000 over 10 years, the difference in investment returns was significant:

Further, if that investment was held over 20 years, the difference becomes more powerful again. This is when the benefit of compound returns comes in as well as time – which is the most powerful asset we have.

If we look at the same investment as above but over a 20 year period, we see the following results:

That same investment over 30 years sees an even more powerful difference:

This example is only taken into account a one-off contribution of $100,000. So you can imagine the difference if we did that same exercise with $500,000. The numbers are obviously going to be a lot bigger. Further, if we add another contribution amount on an annual basis, the compound difference can be huge.

That is why we emphasise with our clients at Emanuel Whybourne that super is an incredibly powerful asset that we as Australians have and it is crucial to make the most of it so that when you do retire, you can enjoy comfort and peace of mind.

If you are looking for superannuation strategies and financial advice to help you make the most of super investments, our team at Emanuel Whybourne would be delighted to meet you.

Contact us today for a brighter tomorrow.

Regards,

Tim

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

NewsLetter

Free Download