Tim Whybourne

December 14, 2021

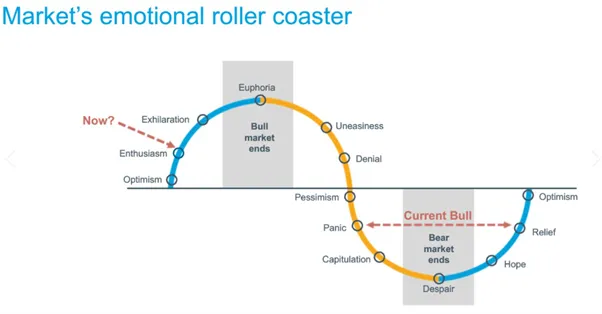

They say the only people who get hurt on a roller coaster are the ones who jump off.. makes sense! This really is the perfect analogy for financial markets as if you look at any financial chart over a long enough time it will look like a rollercoaster ride especially if you look at shorter periods of time. The most important thing you can do is to stay invested through both the peaks and the troughs, like the roller coaster if you try to jump off at the wrong time then chances are you will end up hurting yourself!

This year has been a very strange year indeed. Markets started the year strong even after a record 2020 and from January to February markets were looking good. The rest of the year ended up to be a bit of a rollercoaster ride with some highs, lows and loop de loops but here we are yet again at the end of another year and portfolio balances are teetering around all time highs.

It would not be considered unfair to liken financial market behaviour to the behaviour that my 3 & 4 year old (my wife would probably argue also myself) exhibit from time to time. Just like my kids can be incredibly irrational and fail to listen to their parents, markets can spend most of the year ignoring any signs of danger and not listening to warning signals such as inflation prints and greed index’s but being the irrational beasts they are, this behaviour can turn on a dime and a piece of information that was previously deemed to be irrelevant can then cause markets to sell off. Sometimes there doesn’t even really have to be a reason at all!

I think market performance can much more accurately be predicted by looking at the wave of emotions investors go through as the markets rise and fall … it really is quite predictable but fascinating nonetheless, the trick to managing your emotions is actually to ignore them entirely!

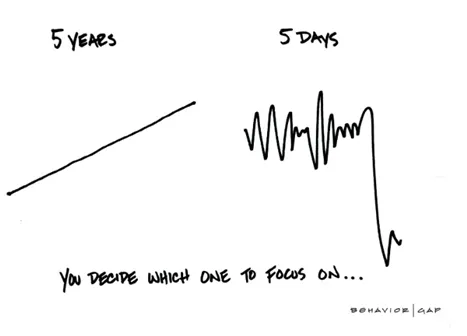

It has been a wild ride this year and we don’t expect next year to be any different but as always, we encourage clients to zoom out when they are looking at their accounts over time. We always say the longer your time horizon the more certainty we can provide over the returns we target. This comes back to my point above that in the short-term markets can be incredibly irrational but given enough time, fundamentals always prevail. In a short amount of time, markets are always going to look volatile but if you can zoom out it will be a much smoother, this is illustrated quite simply below.

It is hard to believe that this is the second Christmas we will be celebrating at Emanuel Whybourne and 2022 will be the second full year of operation. Within our firm we have grand plans for 2022 with several additional staff planned, which will assist us in giving our clients the high level of service that they deserve.

We also have grand plans for our portfolios next year being largely optimistic on how 2022 will pan out. There is one thing I am sure of and that is it will be a stock pickers market, in fact I think that is how the next decade will play out as we see many of the companies that make up the equity indexes as we know it disrupted by smaller incumbents. Some of these companies may be familiar to us now and some of them may not even exist yet, we do think that this will be the decade of disruption with a particular interest in renewable energy infrastructure, digital health and digital disruption.

It would not be right to mention disruption and not to share the views of CathieWood and her investment team at ARK Invest. In a recent broadcast from Cathie she sited that inflation is transitory and that it wont cause a problem for growth stocks over the next 5 years. They did make an interesting observation that when Powell recently implied that they thought that inflation might not be transitory that interest rates went down (the opposite of what is supposed to happen). Her take on that was that the bond market was predicting that inflation wont bite in as bad as the Fed thinks it will, the same thing happened before the GFC in 06/07. Instead, ARK believe that there might be a recessionary scare next year caused by an inventory crisis but this will not persist and growth stocks will prevail. (Source: In the Know with Cathie Wood, Episode XXIII)

They believe that because growth strategies have been sold off so hard in the recent quarter that this is setting the scene for the next 5 years of 40% compound growth.

Credit Suisse is calling 2022 the great transition. They are predicting we are going to be moving from a period of low inflation and sub trend growth to reflation and above trend growth, this should paint the backdrop for attractive returns. In a recent video from their CIO they stated that the economy is going to be re-opening and the global economy should grow at around 4.3%, this is above trend but below 2021. They do see inflation starting to bite in at 3.7% but again this is above trend. (Source: Livewire: Where credit Suisse is investing in 2022)

They see bonds continuing to serve the purpose of protecting from a shock however their base case is that they will return negative after accounting for inflation. They are overweight equities with a preference to keep cash low. They stated that although there is a lot of talk about valuations at the moment, the P/E for the MSCI world is actually lower than what it was 12 months ago because earnings have been so strong. The caveat to their bullishness is that inflation needs to stay moderate, if this is the case then they expect mid to high single digit returns on the index.

Morgan Stanley has a slightly different view in that they think the index should be range bound for the entirety of 2022. They believe that we should expect slightly negative returns from these levels. In contrast to consensus they don’t believe that the Fed will raise rates next year however they also believe that we will see a robust global recovery, moderation of US growth and inflation and more balanced monetary and fiscal policies. They are overweight in US equities, growth, cyclicals and mega caps with a strong preference for active management. (Source: The GIC Weekly: 2022 Outlook: The Great Rebalancing Begins, December 06 2021)

UBS Wealth Management believe we will see strong nominal growth and although Omicron may restrict activity in the near term it will not be a deeper pullback than previous outbreaks. They believe that the strength in developed markets will be enough to counter the underperformance in the Chinese economy. In contrast to the post GFC period they say our incomes are much higher and income growth is much stronger, the unprecedented levels of fiscal and monetary policy have led to much less insolvency and faster rebound in earnings so with borrowing costs still at record lows, business are in a good position to rebound from here. (Source: UBS Asset Management, Panorama: This cycle is different and better).

UBS believe that the Fed are likely to stay with a “do no harm” approach in that they are very aware of the impact their decisions they make have on financial markets so they will try not to rock the boat. They are underweight Australian equities, Neutral US equities and overweight Japan and Europe.

In a recent AFR Article, Bank of America demonstrate that they believe is that the first half of 2022 will be positive with the second half retreating. Stephen Suttmeier, the banks technical equity strategist stated “in our view, the cyclical bull market for US equities from the 2020 COVID-19 low shows signs of its age, this makes for a vulnerable 2022.

In the same article, LPL financial said it sees the S&P500 reaching 5100 by the end of 2022 (from 4684 at 8/12/21), they stated that “we believe that we are currently approaching or are in the middle of an economic cycle with at least a few more years left … if this holds true then we believe the chances of another good year for stock are quite high … interestingly they identified that over a 30 year cycle, the average gain in the S&P500 is 11.5% and of the past 20 years the market was up 80% of those years … the odds are stacked in our favour! (Source: AFR Article: Buckle up for a rocky year for equities: Bank Of America. 8/12/21).

What I am trying to illustrate above is that we have some of the smartest minds in the world commenting on how they think next year will play out and many of those views or polar opposites. This is the case every year because it is impossible to pick one year returns however, I would bet that if you asked for a seven year view, those views would come much closer together.

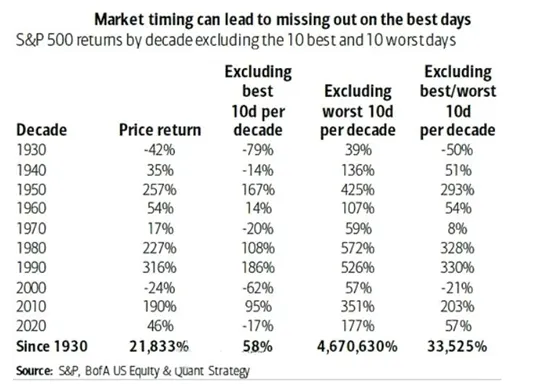

I read a recent anecdotal post from our friends at Ophir Asset Management recently that asked an interesting question. The heading read – “ Want to turn a 21,833% return into a 4,670,630% return? The answer was you just need to avoid the 10 worst days of the market since 1930 … Unfortunately this is impossible and just like you cant avoid the 10 worst days, you cant pick the 10 best days either. The analysis showed that if you missed the best 10 days per decade your return would have shrunk from 21,833% to 58%. The message of the post was to illustrate that “expensive” or “cheap” markets are horrible indicators of future performance and you are going to be much better off remaining invested over the period. Personally I would rather lock in the 21,833% return than to have the potential of throwing away 30 years of hard work.

Source: Ophir Asset Management Linkedin Post

This is consistent with how we think of portfolio management and although we are confident in the direction equity markets over the next year and certainly over the next decade, there will be periods that aren’t as comfortable as others. The key is getting your investment strategy straight from day one and sticking to it, If you don’t fall off the rollercoaster you will arrive at your destination!

This will be my last comment on markets for the year so from everyone at Emanuel Whybourne we wish you all a very Merry Christmas and a Happy & Prosperous New Year and we look forward to continuing our work with you all next year!

Kind Regards,

Tim Whybourne

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

.png)

NewsLetter

Free Download