Charles Troian

Heightened volatility has been the cost of doing business with financial markets for the better part of 18 months. To start the year, we sighed with relief as central banks the world over had seemingly regained control of the inflation spiral. Markets were optimistic and valuations correspondingly began their move away from the pessimistic narrative we have become accustomed too. Enter the modern ‘liquidity crisis’. Over the last few days, headlines have been dominated by the news of several US banks collapsing, followed by increasingly shaky conditions for the European bank ‘Credit Suisse’. Understandably, markets have jittered as central banks assess the real influence of their monetary policy and investors ponder the stability of our global banking system.

Firstly, I’d like to preface this note by stating that we do not believe that the events of last week are indicative of a more systemic issue, or one that will culminate in another Global Financial Crisis. In 2008, problems were borne by asset quality issues and excessive risk taking by banks. In 2023, the problems we are observing revolve around the stickiness of funding (how attractive deposits are), and the duration headwinds to asset prices, specifically bonds. Indeed, the insolvency of Silicon Valley Bank (SVB), Silvergate, and the Signature Bank New York expose idiosyncratic weakness in the system, but not systemic weakness. A liquidity crisis, as opposed to a credit crisis, can be solved by the flick of a switch.

Overnight, we saw that switch flicked on by the Swiss National Bank, as they moved to provide a $54bn loan facility to help Credit Suisse (‘CS’) through its short-term liquidity issues. You might now be wondering, what is creating these liquidity issues, and why is this different for other banks?

In the aftermath of the Global Financial Crisis regulators instituted an internationally agreed set of measures to strengthen the regulation, supervision, and risk management of banks. Significantly, regulators forced banks to hold a large portion of high-quality liquid assets (‘HQLA)’ on their balance sheet, so that they could theoretically meet a stressed deposit outflow for 30 days. HQLA’s can be treasury bonds, high quality corporate debt, and in some cases, Mortgage-Backed Securities (‘MBS’). This regulation effectively forced trillions of dollars’ worth of bonds onto the balance sheet of banks. However, as we have seen over the last 12 months, high quality assets aren’t immune to interest rate risk. For this reason, banks typically hedge against this risk so that asset valuations aren’t exposed to the perils of duration in a rising rate environment. This risk was exacerbated as bonds fell towards the lower bounds of yield and interest rate hedging became incredibly expensive. So, what went wrong with SVB if banks are regulated to maintain appropriate liquidity requirements?

Silicon Valley Bank

The short answer is that they did not hedge their interest rate risk…at all. This wouldn’t be an issue if the bonds were held until maturity, but it is a very real issue for a bank that runs a deposit business. SVB was the 16th largest bank in the US, and unique in the sense that they provided banking services to almost half of all ‘venture capital’, or ‘start up’ businesses in the US. As tightening monetary policy drained credit from the system, funding for startup ventures dried up, forcing their customers to draw on their liquid bank deposits. This resulted in the bank having to realise huge losses on their unhedged bond investments to service deposit outflows. Adding to the realisation of these losses, SVB proposed a common equity raise in an effort to strengthen their balance sheet, which was perceived negatively by the market and depositors alike. The result was a bank run and the consequent collapse of SVB, underpinned by somewhat unique circumstance and poor risk management. So, how did they get away with poor risk management if regulation doesn’t permit? The simple answer is that they’re not considered a ‘big bank’, with assets less than $250bn. This means they are not subject to tighter regulatory scrutiny, such as enforced liquidity ratios or net stable funding requirements that force ‘big banks’ to diversify their funding base and prepare for stressed outflow scenarios.

Now, I’m sure you’re thinking – but what about the other ‘small’ banks? It can be said that SVB’s lack of hedging interest rate risk was unusual, and a point should be made that SVB conveniently hovered underneath the ‘big bank’ classification threshold, all the while lobbying for this threshold cap to be increased. This isn’t a case of ignorance. SVB demonstrated a clear understanding of hedging risk in their 2021 financial reporting, but throughout 2022 as hedging became expensive, opted instead for the use of accounting tricks and a voluntary reduction of their hedges.

‘Moral Hazard’ is a term popularised by the 2008 GFC, and one that polarises bankers for good reason. It defines a situation where a party lacks the incentive to safeguard against a financial risk due to being protected from potential consequence. The Fed moved swiftly to affirm confidence in deposit taking institutions, pledging liquidity to SBV’s deposit clients, and leaving equity holders and senior management out to proverbially dry. In my opinion, this was a clear message that the Fed will ensure confidence to depositors through liquidity, but it will not bail out bad actors such as SVB in a classical sense.

Credit Suisse

As the smoke settles in the wake of SVB’s fallout, the market and media has turned its attention to Credit Suisse. Global news outlets in all their sensationalism have attempted to infer ‘contagion’ in the banking system, stemming from the issues experienced in the US. Whilst CS are also experiencing liquidity issues, the circumstances are not comparable. Credit Suisse is one of the world’s largest banks and is well capitalised, despite operational short falls that have resulted in the deterioration of share price. To put their scale into perspective, they have a market capitalisation of ~$8 Bn, with a balance sheet of more than $500bn. The share price was under significant pressure prior to the events of last week, but now trades at a price to book value of less than 0.20, or in lay terms, a price that is 80% less than its book value! This isn’t necessarily a signal that it presents an investment opportunity, but it furthers the point that the issues publicised last week aren’t indicative of credit stress or deeper balance sheet concerns. So, what’s going on?

For some time now, CS has been dealing with well publicised issues. These issues include poor AML and risk management, that have resulted in significant fines by the regulators, and extend to the implosion of earnings for a business heavily dependent on a healthy M&A environment. Last week, the Saudi National Bank, key interest holders in CS, publicly rejected further investment in the bank. Naturally, this spooked the market and caused the banks shares to fall ~25% in a single trading day. As a result of this sharp move, counterparty risk hedging spiked, and CS’ 1 year Credit Default Swaps (CDS) rocketed. A CDS is an insurance contract that safeguards a banks exposure to their financier. In simple terms, borrowers were concerned about CS’ liquidity. Enter the Swiss National Bank with a $54bn facility, strong armed by the Saudi National Bank comments, to put a fast end to liquidity concerns. This lifeline demonstrates just how easily central banks can resolve issues of liquidity when presented with a candidate who’s balance sheet is appropriately governed by the regulatory measures implemented in a post GFC world.

Adding to the embrace of the Swiss National Bank, CS demonstrated its financial strength by announcing on Friday that it will buy back ~$3bn in senior debt securities that the market considers distressed. Then, over the weekend, rumours of a potential takeover plan by UBS (8x the size of CS by market capitalisation) were broadcasted as yet another act to arrest a collapse in confidence. This takeover was confirmed this morning, with the full support of the Swiss National bank, pledging further liquidity lines to encourage the commercial transaction. Whilst this is an evolving news story, the acquisition of CS at a very low cost with massive central bank support can be seen as positive for all parties to the exception of CS shareholders. Only time will tell how this resolution plays out, but with short term liquidity risks resolved, the next challenge for regulators to look towards is public confidence. In my opinion, decisive action by both the Federal reserve and Swiss National bank towards dealing with these issues, signal an acute awareness of a potential confidence crisis if these issues aren’t addressed swiftly.

Outlook

The rapid constriction of credit as central banks hiked with unprecedented velocity has created challenges for banks in their pursuit to maintain liquidity requirements. We live in a leveraged world that is highly sensitive to the ebbs and flows of credit. A world adjusting to the disinflationary choking of money supply. Whilst liquidity is the risk to financial institutions right now, it is a risk that can be solved with relative ease by central banks. In fact, the Fed has already unveiled a new facility to enable institutions to post bonds as collateral and borrow against them, rather than being forced to sell them at a loss to meet funding requirements. It is critical for the Fed to maintain confidence in the banking system, so to this support we see no end.

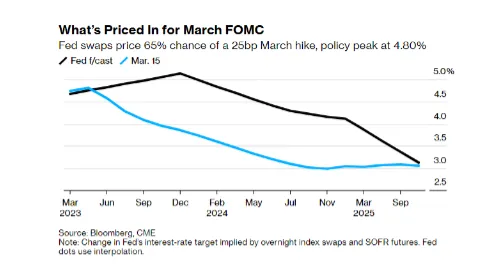

The tremors of this week should not be seen as an indicator of a systemic issue for the global banking sector, but rather a signal to central banks that their efforts to quell inflation are having unintended consequences. Whilst we expect these tremors to influence investment portfolios by way of short-term volatility, we do not expect them to materially impact long term performance objectives. It’s worth noting that we generally limit portfolio exposure to this industry at EW&L. This is despite short term market favour throughout 2022, which has now dramatically unwound. We have written and spoken extensively about our long-term investment philosophy, the irrationality of markets in the short term, and the benefits of staying the course. In my opinion, the below chart demonstrates a silver lining to these live issues, so far as asset pricing is concerned.

Coming into the year, markets estimated a peak US cash rate of 5.70%, and no rate cuts. Following this banking shock, traders are now pricing a peak policy rate of 4.80%, with rates cut to below 4% by the December meeting. The key driver of share market returns in 2022 was the rapid increase in cash rates by the Fed, so we expect that the unwinding of tight policy may be a positive catalyst for share prices, particularly for long term ‘growth’ assets that are ultra-sensitive to these changes. If nothing else, the rapid re-pricing of terminal rate expectations demonstrates just how fast conditions can change in the short term, amplifying the importance of taking a long-term approach to investing.

In any case, we believe that the liquidity issues the banking sector faces are resolvable, short term, and importantly, starkly different to 2008. Investors with a well-diversified portfolio and a commitment to their long-term strategy will ride the waves of this shock, as the market has repeatably done in its ascension to new heights.

Kind regards,

Charles & Mitch