Craig Emanuel

December 14, 2022

Let’s try to make sense in this investment World, which is well ahem, non-sensical. We toasted in the fresh New Year of 2022 with a sense of optimism. The World 11 months ago was humming along pretty well. We all learned to live somehow with Covid. You could borrow money for nothing, inflation was under control, no war existed.

As the year 2022 played out, every asset class fell in value. Significantly. I emphasise ‘every’ asset – as this is a very rare event indeed. 2022 will go down as a memorable year in history. Ironically, not necessarily a year that investors will want to remember.

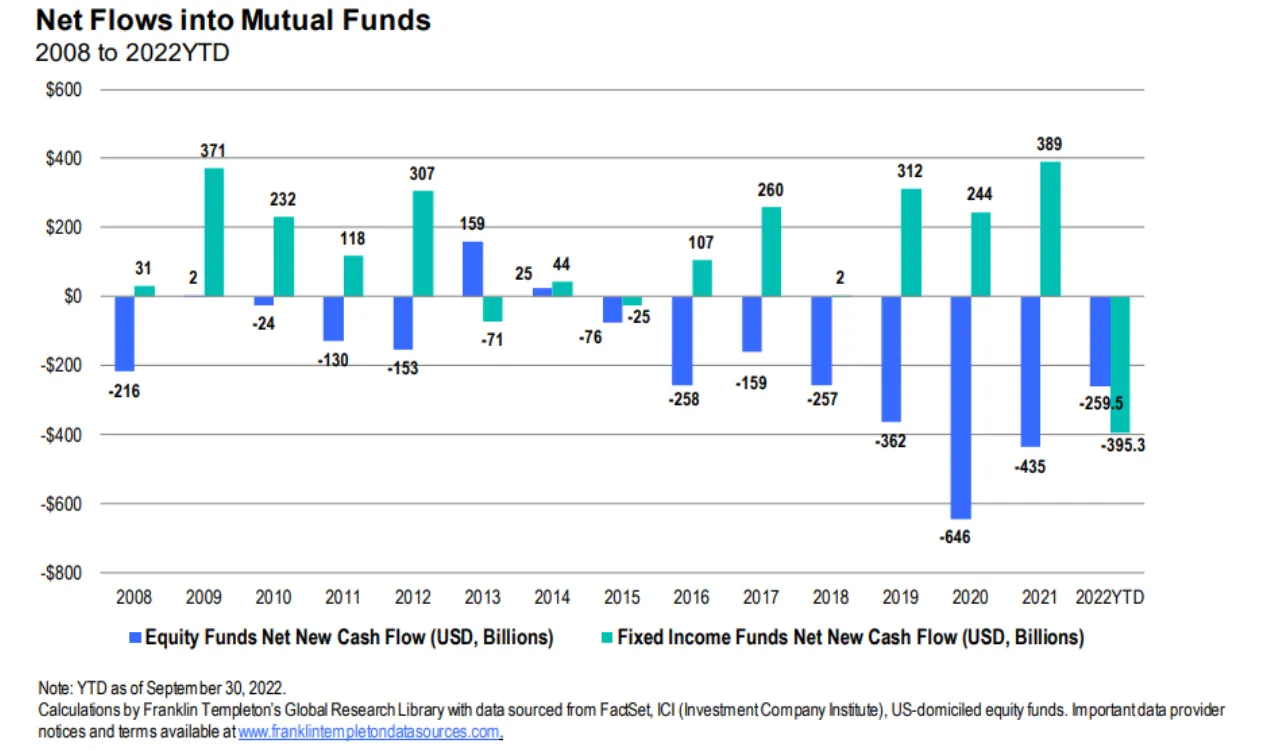

For portfolio construction, the supposed secret blend of ‘stocks and bonds’ for the first year in long time didn’t work. The theoretical ‘balanced portfolio’ model formally broke during 2022. The worst first half of the year for equities since 1960. The worst return year ever for the bond market. Growth assets didn’t grow, and defensive assets didn’t act defensively. (Refer the chart below – not even during the GFC did we experience the mass fund outflows of investment funds globally seen, then during 2022):

During 2022 journalists around the World became economic professionals at explaining the risks of ‘sticky inflation’. How many million tonnes of timber are exported from the Ukraine, which no-one really cared about until 2022. Two new words became inseparable during 2022 – ‘Fed’ and ‘pivot’.

So, I’m hoping I no longer see the words ‘Fed’ and ‘pivot’ used together during 2023. Nor am I losing sleep waiting to hear if the US Fed or the ECB will act as a ‘dove’ one month or a ‘hawk’ the next month. If the World’s central bankers act as a nice bird or a naughty bird won’t make any difference to any of your long-term investment returns. This all means zippo.

We’re all facing a new era and a new economic reality, which will continue to see the World’s central bankers hike up the cost of cash to choke inflation. At the detriment of the economy. Central bankers will be effective, as they always have been.

This in time, will reduce everyone’s spending. This has and will continue to reduce our wealth. It will sadly result in millions of job losses globally. Countless companies filing for bankruptcy. Not just fraudulent crypto exchanges. We are now facing a global recession. This is no secret. The public and investment markets are very aware.

Recently the partners and analysts of EWL have had some amazing opportunities to attend several domestic and global investment summits, speaking and meeting with a selection of the World’s largest investment managers, from credit and fixed interest, through to alternatives, property, global equity, and venture capital.

We were fortunate enough to meet in our boardroom the founder/CEO of the World’s largest private equity fund Hamilton Lane (Mario Gianinni, who personally manages $1.4Trillion), the head of each asset class for JP Morgan in Singapore, a private dinner with the Global CIO of T Rowe Price (Sebastian Page) who oversees US$1.3Trillion in assets, through to the World’s most renowned distressed asset investor, Howard Marks.

Our staff absolutely love being involved in high level debating surrounding the just how this year compares historically to that of similar previous cycles. If there is any close comparison! Critically, what potentially lies around the corner for the global economy, investment markets and most importantly, for our clients. As investors, what lies in wait for the year ahead?

There are so many variables, and cross currents impacting financial markets now. Multiple financial levers pushing and pulling economies, currencies, and markets in opposing directions. Trying to understand if the market is currently cheap, has further to fall, or if inflation has peaked, if central banks will announce monetary easing doesn’t matter over the short-term. These are answers that frankly, no one has. Central banks don’t know where the neutral rate is or how high rates need to do – we witnessed this year to date. Earnings multiples are based on historical data. What looks cheap or expensive can change based on future earnings growth (or decline) and setting expectations for earnings is certainly easier over a longer time horizon, as opposed to quarter-to-quarter swings from pandemics, inflation, rates, or conflict. If you’re trying to ‘trade’ or as we term it – ‘speculate’ on these markets and somehow make money, it’s either pure luck or you are a clairvoyant, according to Ray Dalio.

We’ve just lived through a fundamental asset re-pricing era. Since public (listed) markets being forward looking and liquid, they have born the immediate pain of this re-pricing. Now comes the time for private market assets (such as unlisted property and private businesses) to experience a very similar painful downward price adjustment. Over the coming 6 to 12months, the cost of money will continue to rise at one of its fastest pace in history – forcing next gen investors to realise that borrowing money for nothing isn’t normal. Although inflation globally has peaked, interest rates may not be reduced until 2024 according to some investment houses (consensus view, Credit Suisse Outlook 2023). Our view is that is we will get clarity on monetary policy through Q1, Q2, 2023 as corporate earnings announce the impact or potential impact of higher rates (which lag and take time to flow through). In a recession, or period of negative economic growth, we expect either a pause, or a cut to rates, which would be positive.

2022 forced investors to yet again, adopt a varied investment approach. Instead re-allocate to yield investments (those paying out most of their earnings). To revisit the importance of alternatives (non-correlated assets) within an investment portfolio. Most importantly to not pay overs for future earnings growth yet to be realised, particularly in an environment of economic uncertainty.

Inflation itself is not a bad thing. Inflation is needed within an economy it’s typically a signpost of economic growth. As the economy increases productivity, the economy grows, wages go up, price increases can be passed on. So, inflation is usually a good thing – but when it runs too hot, or goods and services inflation outpaces wage growth for too long – this becomes problematic. The stage is being set currently for the next economic supercycle.

Economic cycles naturally create tailwinds to asset prices. This has and always will be, the basis for global economic expansion. The headwinds of 2022 are far from normal and will disappear. Not one economist will correctly predict when.

Central banks will eventually gain traction on inflation and declare their truce. According to JP Morgan, the vintage of 2023 for growth investors will be one of the best of the last decade, with returns across asset classes and the ’60-40’ portfolio moving significantly higher than recent years.

Investing is never easy. Investing is not for the faint hearted. Years such as 2022 tested both advisor’s nerves and our client’s nerves. We’ve consistently advised ‘do not time markets.’

You may be completely lucky timing your exit with the market high, however where investors can also destroy capital is in attempting to timing the re-entry. As an investor – you don’t want to miss those ‘up’ days. You can’t afford to miss the recovery. It’s the recovery events which provide you with the bulk of your long-term returns. Simply missing 10-15 of the best trading days in a year can completely erode the market return, if not see your portfolio end up in the red.

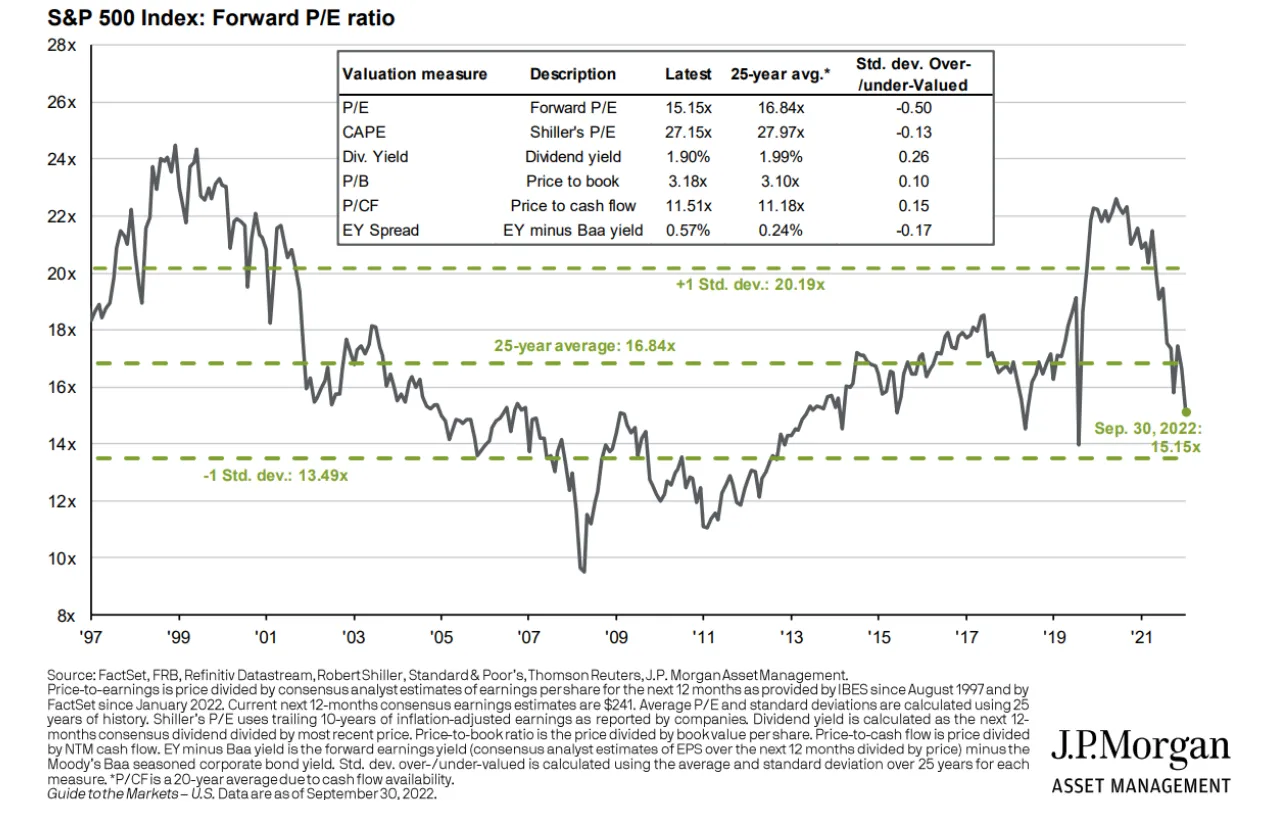

When we look back at the year which was 2022, history will yet again prove that 2022 was one of periods that provided investors with a historic investment opportunity. With that said, 2022 was unusual – with rates moving from zero, bonds and equities couldn’t function as they normally would. There was no cushion to volatility, given bonds became ineffective in their role to do so. Now, we have a wider toolkit. One where bonds can act defensively, provide a reliable yield, and equities are moving off a valuation that appears attractive by historic standards, but at the very least, is 20-30% cheaper than where it traded a year ago (peak to trough).

Until we’re able to look back at 2022 in hindsight, sadly investors can only see the daily, weekly, and monthly worrying economic data and frightening volatility. It won’t be until after the recovery that economists will promote their ‘I told you so’ views that the market was a fantastic opportunity.

Thinking optimistically and investing with caution sounds counter-intuitive. Because it is. History is not destiny. The road ahead is never clear.

The past several years have been year full of ‘Black Swan’ events. Pandemics, supply-chain disruptions, decades high inflation, rates trading at zero for bonds and a major conflict in the Ukraine. My advice for 2023 is to instead be prepared for the White Swan events. White Swans are even harder to predict…

Until next time, Craig

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

.webp)

NewsLetter

Free Download