Tim Whybourne

August 31, 2022

Did you know that they now teach five years old’s how to code? This means that some children are learning to code before they can tie their shoelaces! On that note, I always find it fascinating how quickly children can navigate their way around an iPad or iPhone whilst some elder generations find it difficult to find the “on” button. I find myself somewhere in the middle; I’m competent but certainly not an expert, and I attribute this entirely to the generation I grew up in.

Every generation is brought up slightly differently as the world does change and we all grow up in different times. If you were brought up in the 40’s that was very different to growing up in the 70’s and the 70’s were very different to growing up in the 90’s. My own children are growing up in what I consider to be very different times to when I grew up. They would have no idea what to do with a video player, a rotary phone, a discman or a Gameboy. When I was growing up, every photo was treasured as each click came with a considerable cost to develop. My children’s lives are documented in photo nearly by the hour with the invention of the phone camera, stored in the cloud for eternity.

Technological disruption has been going on forever, from the cavemen discovering fire, to 3D printing replacing traditional manufacturing. However, I am of the strong belief that the rate of change has accelerated, and we are in the midst of a digital revolution. A revolution that will have profound impacts on the world as we know it and consequently how we invest.

Last week Craig, Ryan and I had the privilege of attending the Portfolio Construction Forum in Sydney. An opportunity for 40 of the worlds most esteemed fund managers and policy makers to come together and provide a good cross section of their views on markets and where they are heading. One of the first speakers to take the stage was someone I have heard speak several times in the past and never tire to hear from, Bernard Salt. Bernard is a renowned demographer, who’s job is to research the composition, distribution, and change/trends in human populations over time.

Bernard’s opening statement was that Australia will be a very interesting place to invest over the next 10 years, or that the demographics will at least be in our favour.

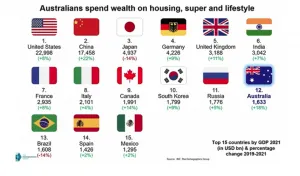

One of his key observations was that Australia has come a long way in the wealth ranks this year, moving up from in the 20’s to the 12th largest economy on the planet. This is just behind Russia at number 11, and ahead of Spain and Brazil for the first time.

The interesting thing to point out is that there is no country on this list with a lesser population, meaning we are very rich per capita. So where do we spend our wealth? Not on military adventurism like some of the other G20 nations, but housing, quality of life, superannuation, and travel.

This is why you would bet on Australia over the next 10 years!

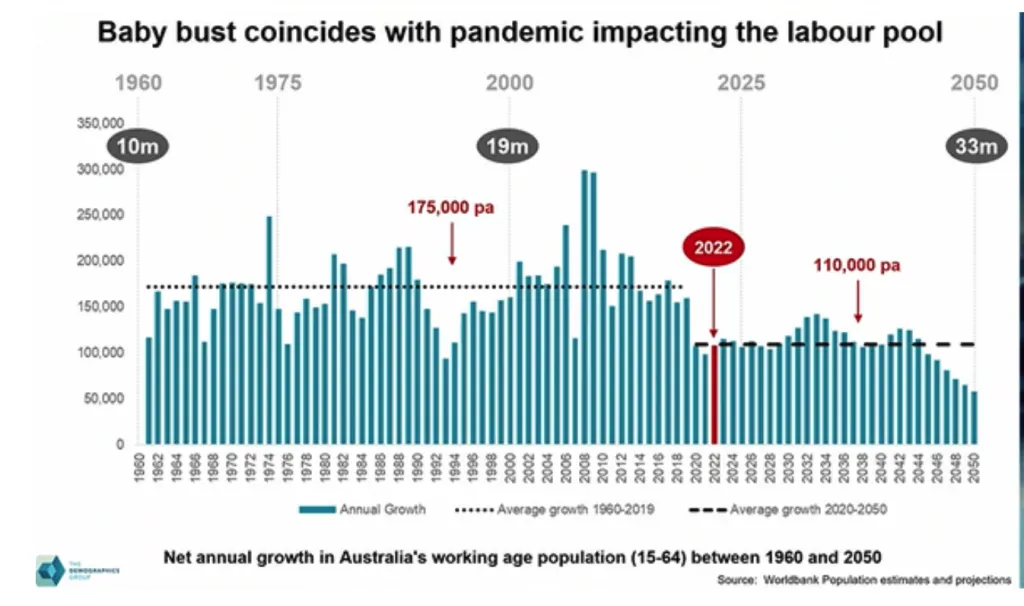

The chart below shows the number of people added to Australia over the past 70 years in the 15–64-year-old bracket. Importantly, this is the age bracket that reproduce, take out loans, pay tax and buy consumer goods. This demographic has been the engine of the consumption market for the past 7 decades.

Historically, Australia adds about 175k people per year on average to this bracket, which includes a lot of skilled immigration. This is one of the main reasons we have traditionally had such a strong construction and housing sector. Following the downward trend of immigration statistics, Bernard expects this figure to decline by 31 percent, with 55k less people being added this bracket annually. This is a problem.

According to Bernard, just as there was a Baby boom in the 1950’s, there will be a Baby bust in the 2020’s, when the boomers exit at age 65 and the millennials enter at 15. This is now happening at the same time we closed our borders to immigration, so the pools of labour are shallower than they should be.

This change is important to highlight, as an economy with less labour to draw from will require more efficiency per unit of labour to run optimally. In Bernard’s words ‘digitisation’, ‘mechanisation’, ‘roboticization’, artificial intelligence and ‘application’ to name a few will be the key to increasing productivity and continuing to thrive, not only as a nation but as a global economy. Indeed, this change doesn’t just apply to Australia, it also applies to New Zealand, Canada, US, Europe, and Japan. In my mind this makes the case for investing in disruption stronger than ever.

Historically, the secret weapon for economic growth in Australia has been immigration. In fact, 27% of our population was born overseas. We have added around 150k people per year from immigration, and this has bolstered consumer demand.

Another interesting chart that Bernard discussed demonstrated population flows over the past 120 years (see above). We had not lost people from the Australian continent since WW1, but during Covid we saw net outflows of nearly 100,000 people from Australia. This can’t happen without scarring the Australian population, so we can expect to come out of this differently!

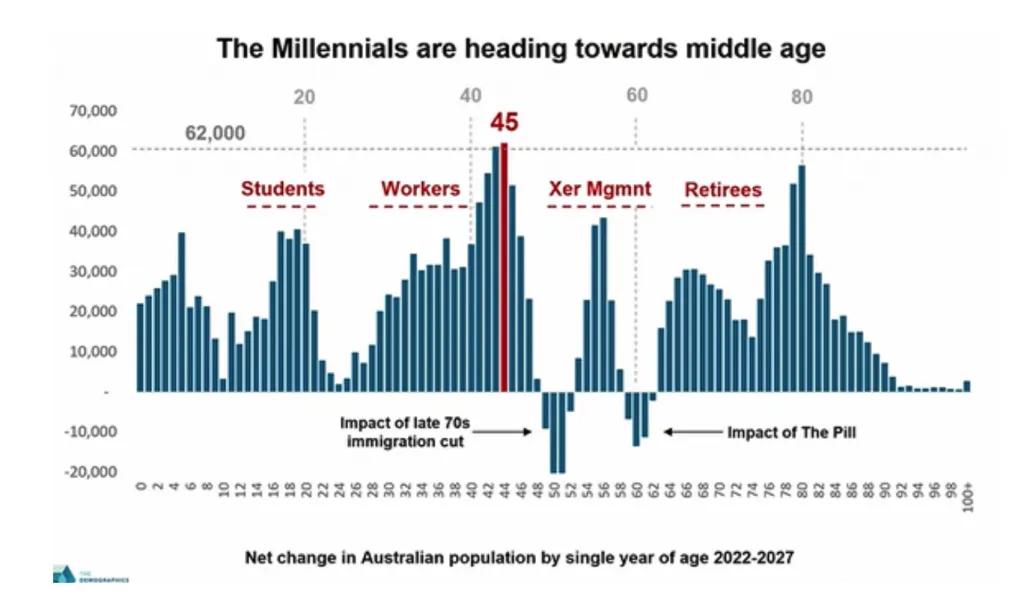

Over the next five years the one thing that stands out is the single year age bracket that is set to explode. There is expected to be another 620,000 people added to the 45-year-old bracket. Importantly, 45-year-olds are the first wave of the millennials and tend to have a strong willingness to spend. Typically, in your late 30’s to early 40’s you may have ‘partnered up’, had one or two or three kids and live in the inner-city sheik apartment in Surry hills, but this just simply doesn’t do it anymore. You need bigger houses with a front and a back yard and now …a ‘zoom room’. There is a demographic shift in demand for suburbia! This has driven demand for property in suburbia and everything it takes to furnish a bigger house.

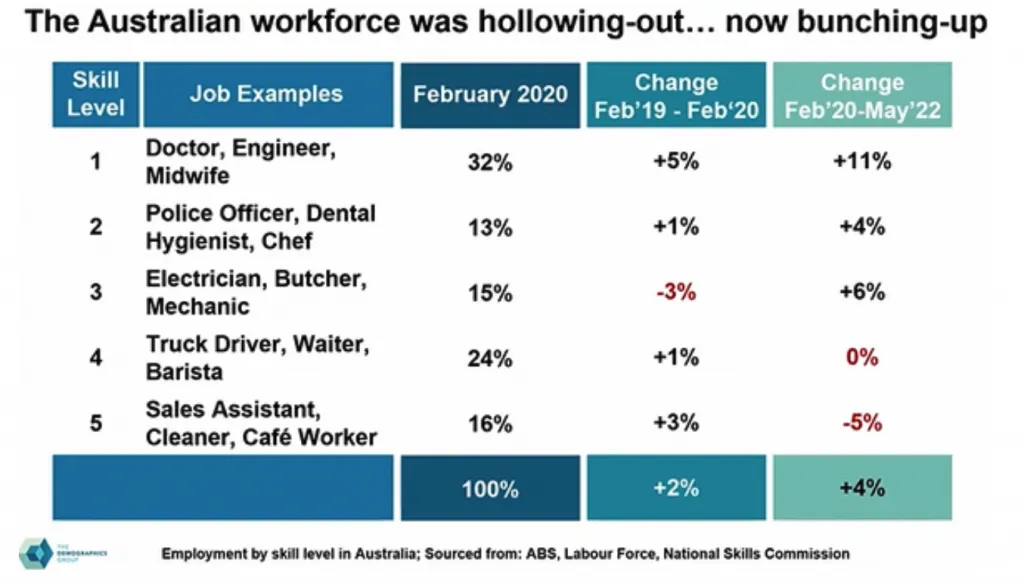

Another interesting remark that Bernard made was around the declining number of lower skilled workers during Covid, as people either left the workforce or trained their way up the job matrix. There has been a ‘skillification’(in Bernard’s words again) of the Australian workforce.

Bernard believes that this has occurred as many people used Covid as an opportunity to upskill, which has resulted in many of the unskilled jobs declining in number whilst skilled jobs and higher paid jobs have increased. This has meant that there will need to be a technology solution to fill the gap for that unskilled labour given as much of the traditional workforce has moved on.

An example of this is, as Bernard phrased it, is the great ‘applification’. He claims this will be one of the great sources of productivity over the next 10 years. A great example of this is the Covid Safe app, an app that cost $21,000,000 to develop according to newspaper reports. It was supposed to save us from the pandemic but was broadly perceived as a disaster. However, there was a silver lining.

Five years ago, the baby boomers didn’t know what an App was. When they had to download the Covid safe app they got their millennial kids to do it for them. They then got the chance to see how easy that was, and this led them downloading apps themselves. Apps are now part of their daily life.

Another example he used was ‘Hotdoc’, an app that helps you book an appointment with your doctor. He found this app when trying to book an appointment with his own doctor and found it to be very easy to use and wonders why he hadn’t ever used it before. It essentially replaces the receptionist and allows you to choose a timeslot to see your doctor or any other number of doctors on the platform. Doing the math, ten doctors at twenty appointments a day equals one thousand appointments a week. One thousand appointments a week at three minutes per appointment to book would essentially eliminate three paid receptionists from the practice to then be redeployed in other parts of the economy where demand lies.

What I took from this was that there will continue to be huge changes made to the way we live over the next decade. From an investment perspective, we want to be exposed to the themes such as automation through robotics, artificial intelligence, ‘applification’ and digitisation to name a few.

The investible theme of ‘disruption’ is not a new idea and in my lifetime alone I have seen huge changes in technology.

A few of these changes can be seen in the following charts.

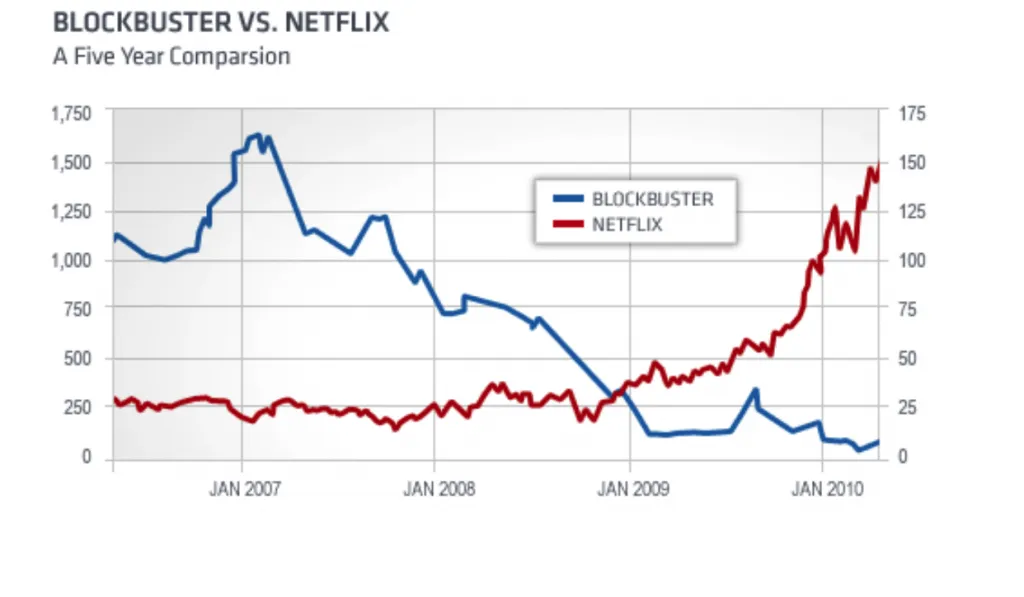

I remember fondly visiting the video store as a kid, not in my wildest dreams did I ever think that an online subscription-based movie service would have replaced the bricks and mortar stores, but here we are.

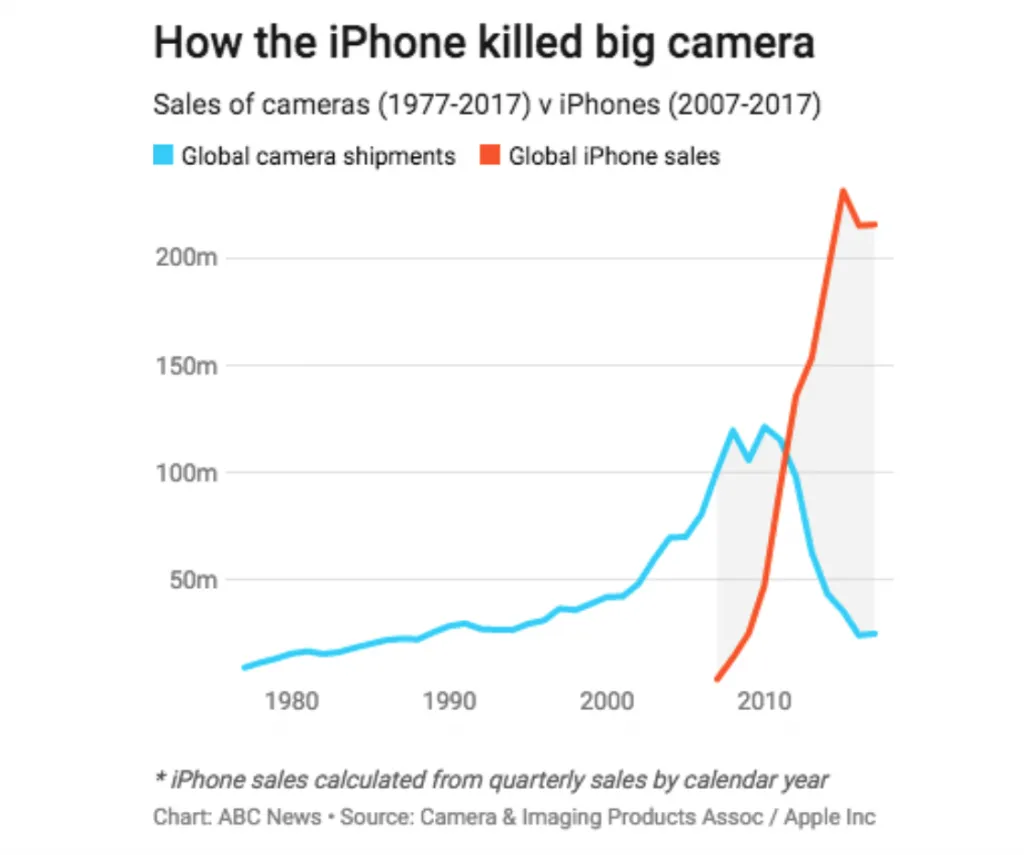

I also remember asking my mum and dad to buy me a camera as a teenager… who knows what my kids will be asking for by the time they get to that age.

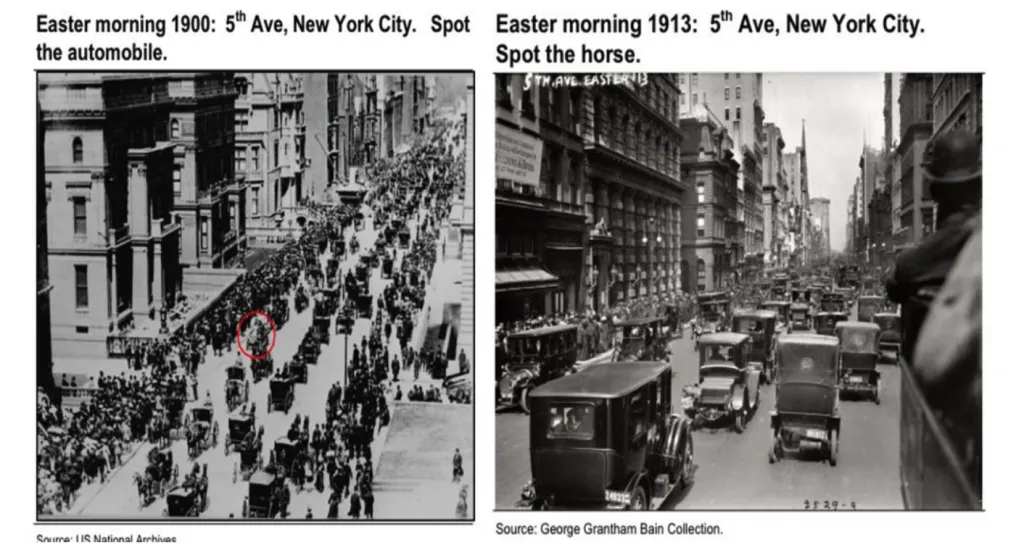

The photo below shows one of the main streets in New York in the 1900s. You can see below a series of horse and carts.. the circled photo is a single automobile. Fast forward 13 years and there is not a single horse in the same photo.

I think investing in disruption over the next 10 years is a no brainer (because…the rate of change is occurring at an accelerated pace, supply chains are being forced away from low-cost labour to automation and onshoring and this will continue to create risks for incumbents, but opportunities for those with optionality / some exposure to innovation. However, it is the short term that is taking everyone’s attention at the moment with huge waves of volatility. This is simply because of interest rates, which change the ‘present value’ valuations of assets.

Investing in disruption or growth often comes at the expense of accepting lower short-term returns (earnings), and instead spending a higher proportion of funds on R&D, improving service and efficiency. Yet when established businesses lag behind these innovators, allowing years or decades of accelerated innovation – they often can’t catch up. Two recent examples are Tesla – with market lead on electric vehicles and Moderna, with a market lead in mRNA vaccines etc.

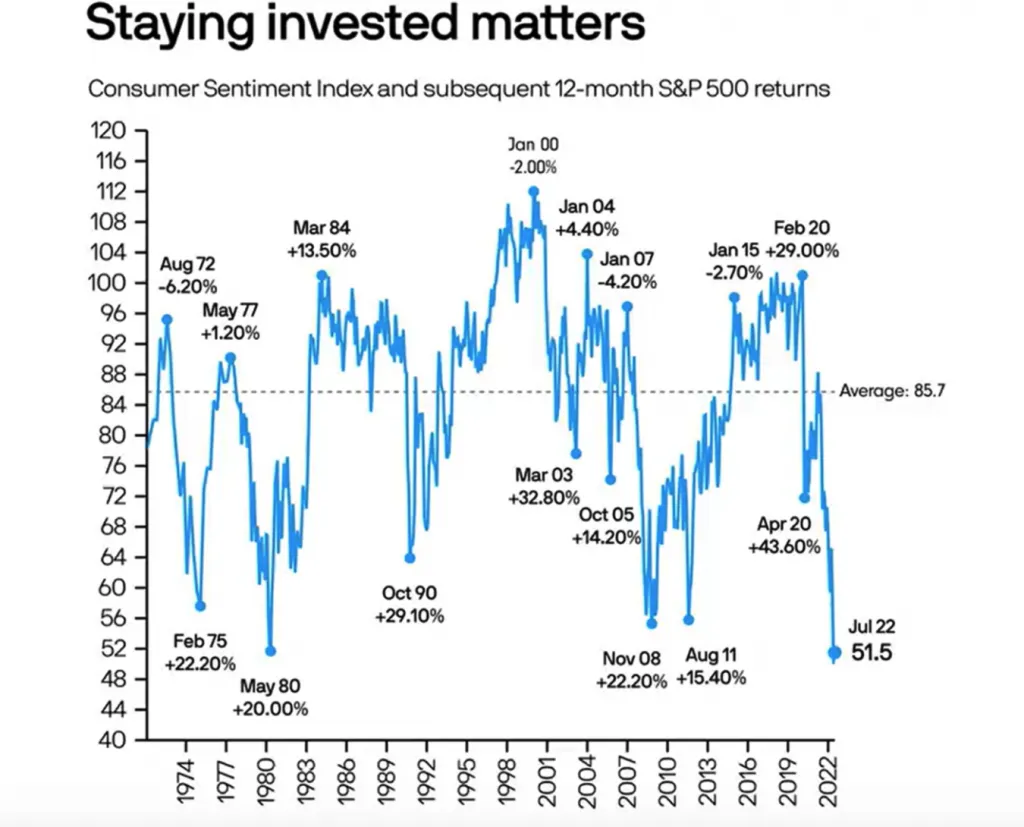

We have seen moves like this in markets before and have come out the other side several times over the past 15-20 years and we don’t believe this period is any different. It is during times like what we are going through now that make it more important than ever to stick to your investment strategy. The chart below illustrates the adage that it is always darkest before the dawn. Historically, markets have returned strongly as consumer sentiment bottoms, so just as things feel like they can’t get any worse, they often can’t.

Until next time,

Tim.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

The information in this podcast series is for general financial educational purposes only, should not be considered financial advice and is only intended for wholesale clients. That means the information does not consider your objectives, financial situation or needs. You should consider if the information is appropriate for you and your needs. You should always consult your trusted licensed professional adviser before making any investment decision.

Emanuel Whybourne & Loehr Pty Ltd (ACN 643 542 590) is a Corporate Authorised Representative of EWL PRIVATE WEALTH PTY LTD (ABN: 92 657 938 102/AFS Licence 540185).Unless expressly stated otherwise, any advice included in this email is general advice only and has been prepared without considering your investment objectives or financial situation.

There has been an increase in the number and sophistication of criminal cyber fraud attempts. Please telephone your contact person at our office (on a separately verified number) if you are concerned about the authenticity of any communication you receive from us. It is especially important that you do so to verify details recorded in any electronic communication (text or email) from us requesting that you pay, transfer or deposit money, including changes to bank account details. We will never contact you by electronic communication alone to tell you of a change to your payment details.

This email transmission including any attachments is only intended for the addressees and may contain confidential information. We do not represent or warrant that the integrity of this email transmission has been maintained. If you have received this email transmission in error, please immediately advise the sender by return email and then delete the email transmission and any copies of it from your system. Our privacy policy sets out how we handle personal information and can be obtained from our website.

.webp)

NewsLetter

Free Download